What is pre-qualification?

Pre-qualification is typically the first, lighter step in the mortgage process. You provide a lender with a general overview of your finances — income, assets, debts — usually through a simple online form or a brief phone call. The lender takes that information at face value and gives you a rough estimate of what you might be able to borrow.Key point: No credit check is run (or only a soft inquiry is made), and no documentation is verified. It's an educated guess based on what you've self-reported.

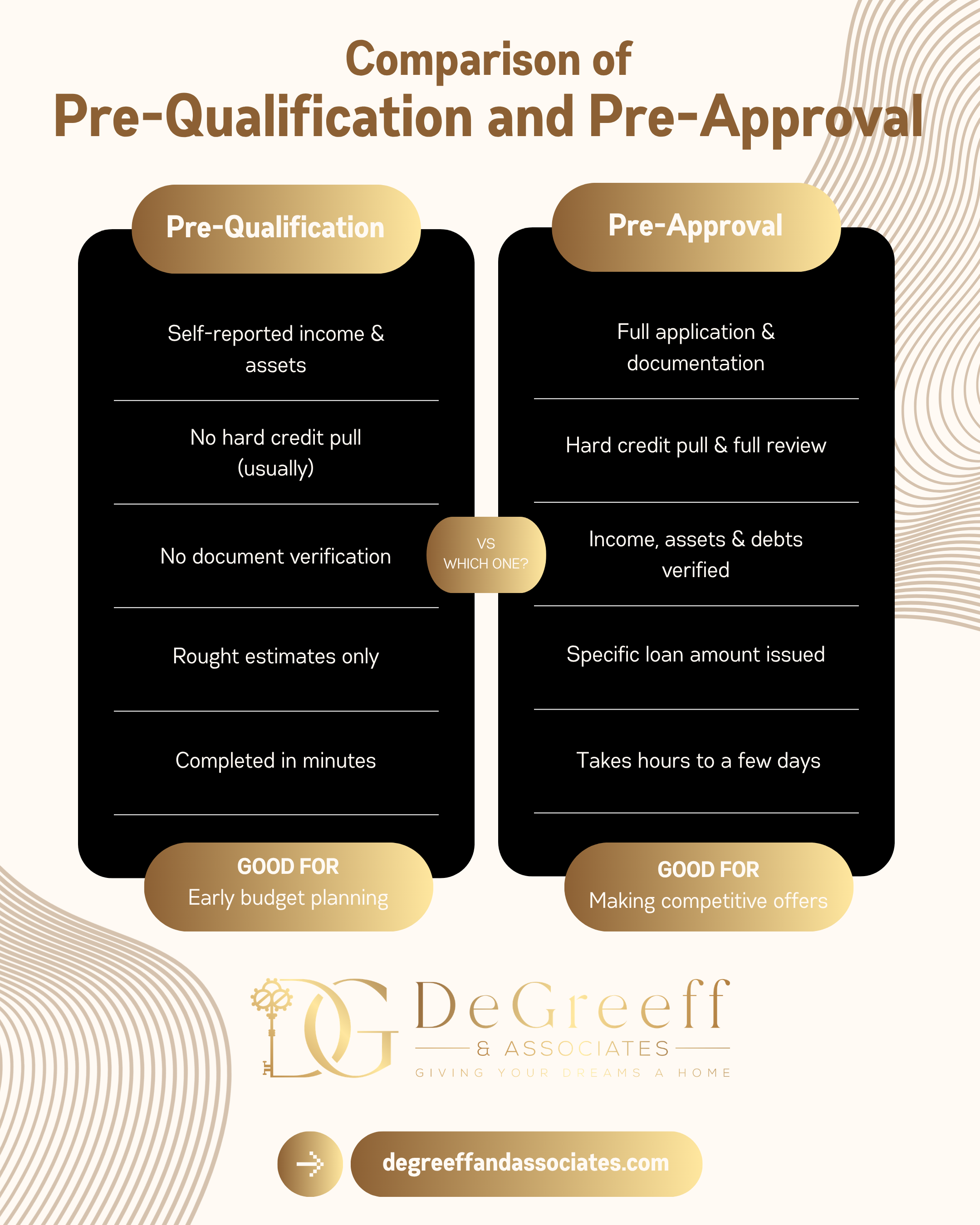

Pre-Qualification

The Quick Snapshot

- Self-reported income & assets

- No hard credit pull (usually)

- No document verification

- Completed in minutes

- Rough estimate only

- Limited weight with sellers

Pre-Approval

The Real Commitment

- Full application with documentation

- Hard credit inquiry

- Income, assets & debts verified

- Takes days (sometimes hours)

- Specific loan amount stated

- Carries real weight with sellers

What is pre-approval?

Pre-approval is a much more thorough process. You submit a formal mortgage application along with supporting documentation — W-2s, tax returns, pay stubs, bank statements — and the lender pulls your full credit report. An underwriter (or automated underwriting system) actually reviews your file and issues a conditional commitment to lend up to a specific dollar amount.Think of pre-qualification as a lender saying "sounds good to me." Pre-approval is them saying "we've checked, and you're conditionally approved for up to $X."

Why this distinction matters in a competitive market: When a seller receives multiple offers, they're looking for signs that a deal will actually close. A pre-approval letter tells them a lender has already vetted the buyer. A pre-qualification letter tells them almost nothing — and savvy listing agents know the difference.

Which one do you need?

For serious home buyers, pre-approval is the standard. Here's when each makes sense:1. You're just exploring — start with pre-qualification

If you're 6–12 months out from buying and want a general idea of your price range, a quick pre-qualification can help you set expectations without impacting your credit score.

2. You're ready to shop — get pre-approved

Before you tour homes or work with an agent in earnest, pursue a full pre-approval. You'll know exactly what you can afford, and you'll be positioned to move fast when the right home comes along.

3. You're ready to make offers — verify your pre-approval is current

Pre-approvals typically expire in 60–90 days. If your search stretches longer, you may need to refresh your documentation with the lender before submitting an offer.

4. The market is competitive — consider a fully underwritten pre-approval

Some lenders now offer upfront underwriting, where your file is fully reviewed before you've even found a home. This "credit-approved" status is the strongest position a buyer can be in and can even allow you to waive financing contingencies in some situations.

Common questions buyers ask

Does getting pre-approved hurt my credit?

A hard credit inquiry from a mortgage application will temporarily lower your credit score by a small amount — typically less than 5 points. If you apply with multiple lenders within a short window (14–45 days, depending on the scoring model), those inquiries are often counted as a single pull. Shopping around for the best rate is worth it.Can I get pre-approved before choosing a lender?

You should apply with at least two or three lenders and compare loan estimates. Interest rates, origination fees, and loan products vary — and even a small rate difference can mean thousands of dollars over the life of a loan.What if I'm pre-approved but my financial situation changes?

Don't make any major financial moves — new credit cards, large purchases, job changes, or moving significant funds — between pre-approval and closing. Lenders often re-verify your information before finalizing the loan, and changes can jeopardize your approval.The bottom line

Pre-qualification gives you a starting point. Pre-approval gives you a competitive edge. In a market where well-priced homes receive multiple offers quickly, walking in with a strong pre-approval letter — or better yet, a fully underwritten approval — tells sellers you're serious, qualified, and ready to close.At Degreeff & Associates, we guide buyers through every step of this process. If you're ready to start your search or want a recommendation for a trusted local lender, reach out — we'd love to help.